|

�

Archives

September 2021

Categories

All

|

Back to Blog

It is the year 2056, I am age 62 and have just retired. I have paid off my mortgage, I have healthcare coverage and I need £3000 per month (net tax) to be happily retired. Research has shown that UK retirees need around this amount to maintain a certain comfortable lifestyle that allows for some luxuries likes holidays, fine dining and more.

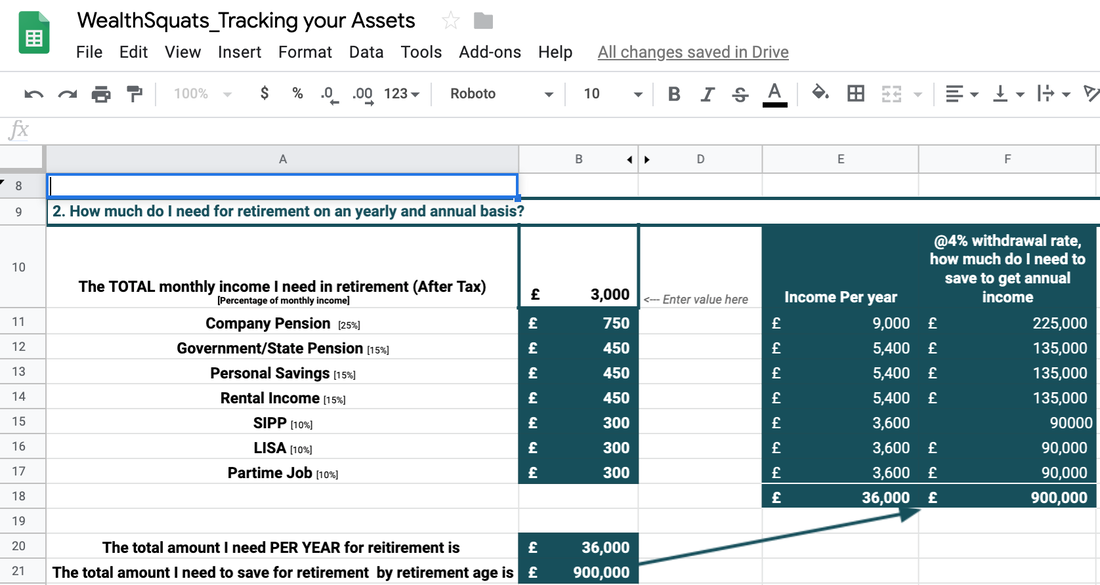

Why did I choose £3000 as my happily retired monthly figure? At 62, I envision a life where I can spend on luxuries, management my expenses and retain or increase the lifestyle that I had when working. An undesirable scenario for me is a position where I am used to a certain lifestyle and then in retirement, I find that I have to downsize significantly. So if I was living on £2500 while I working, In retirement, I don't want to have only £1,500 as income. Studies show that most retirees want there income to be around 70% of their working income in retirement. My £3000 will cover, healthcare, bills, food, clothing, travel, donations and a few luxuries. It is very crucial that my mortgage is paid off or at least close enough to being paid off (2 years away). This way, I will not have to work to discharge the loan or feel the stress of using my savings to cover meet my debt obligations. My ideal situation would be to have my primary home paid off and to have a rental property where I can continue to hold assets. We are likely to live longer and with a retirement age at 62, I can expect to live till I am 85 or longer. This means that my income must last for at least 23 years.  What is your aspirational lifestyle at retirement? My income at retirement will change from getting a whole UNSCLICED PIZZA on day 1 to getting different pizza slices on different days Today, I work for a company and each month on a specific date, I get a salary. That salary is provided once and it funnelled into my expense, savings and investment. Fast forward to age 62, my retirement age. My income will no longer come at a specific date but it will come from different sources to make up £3000. It could look something like this: £750 from Company Pension received in on 8th of each month £450 from State Pension received in on 8th of each month £450 from Personal Savings account received in on 8th of each month £450 from rental income received in on 15th of each month £300 from SIPP received in on 17th of each month £300 from LISA received in on 17th of each month £300 from part-time job received in on 23rd of each month This reconfiguration of my potential income at age 62, changes the way I think of a pay-check. It will mean that for instance, I'll have to organise my spending not around one date but multiple dates. This is a mindset shift that I have to be aware of and start getting use to as the retirement age comes closer. The above is an example. The £3000 I estimate is for an individual. If that amount covers a couple, adjust your income sources to reflect your cirumstance. umm Did I say £900,000? Now that I know how much I want to live on at 62, I now had to figure out how much I needed to save in order to get £3000 monthly. See the table below for full details. To estimate how much I need to save, I learn of the concept of '4% drawdown rate'. This the rate at which I can take out of my savings in order to maintain my pension pot and not run out of money. Let's take my LISA, each month, I need £300 from that account to live on. In 1 year, I need £3600 = £300 x 12. If I want to withdraw 4% of my LISA account at 62, I need (£3600/4% = £90,000 saved in my account upon retirement. So the Ideal scenario is that my LISA will grow annually at 4% and if I withdraw 4% annually, I actually NEVER run out of that £90,000 saved. This is called the natural yield. So if my annual income i £36,000 net, I need (£36,000 / 4%) = £900,000 saved at the age of 62 to maintain the lifestyle I desire. This calculation is based on a number of assumption related interests rates and inflation. However, it gives me a view of the size of the pension pot I'll eventually need. Seeing this figure, I can spend all the £900,000 in 25 years (£900000/£36000). However if I anticipate that I will live longer than 25 years, I need that £900,000 to last much longer.

Want to simulate your pension pot? Have a go at the Wealthsquats calculator shown in the table above. Alternatively you can do a quick search and find other like the People Pension calculator At what age can you access your pension? For each of the pension sources I have mentioend above, you'll need to keep in mind when you can actually start to withdraw from them. For instance, the age when you can access State Pension will differ depending on your birth year, so if that age is 68 years, and you wish to retire at 55, you'll need to find ways to cover the income you would have received from our state pension. So part of my pension plan is looking at the age and time when I can access these income sources. Some Interesting things I found out:

Know the Pension Carry forward rule. I learnt this from a friend. Every year I put in £40,000 into my pension this is the maximum annual allowance permitted by the government. I also manage my wife’s finances and she currently has around £160,000 in her pension pot. For the years where we do not put the full pension allowance, I use the pension carry forward rule where in a given year, I can pay the difference from the annual allowance for the past 3 years. This looks like this; Year 2016 I contribute £30,000 into my pension (I have £10,000 left for my annual allowance) Year 2017 I contribute £20,000 into my pension (I have £20,000 left for my annual allowance) Year 2018 I contribute £20,000 into my pension (I have £20,000 left for my annual allowance) Year 2019 I contribute £40,000 into my pension (I have maxed out my allowance, nothing is left) In 2019, I can contribute a total of £90,000 into my pension because I am able to carry forward £10k+20k+20k= £50,000.  Know your pension status! I want to get my pension situation sorted

There are many variables that impact your growth and longevity of your pension pot. Keep these in mind when reviewing your circumstance.

What you can do now?

Options avaliable for you

More information Read our full guide on pensions here to get started. I also found this website from The People Pension to be useful.

1 Comment

Back to Blog

Recently I came across a new idea called Bond Ladder which allows investors like us to arrange our bonds in ways that provides flexibility with regular returns. This can be an attractive option if:

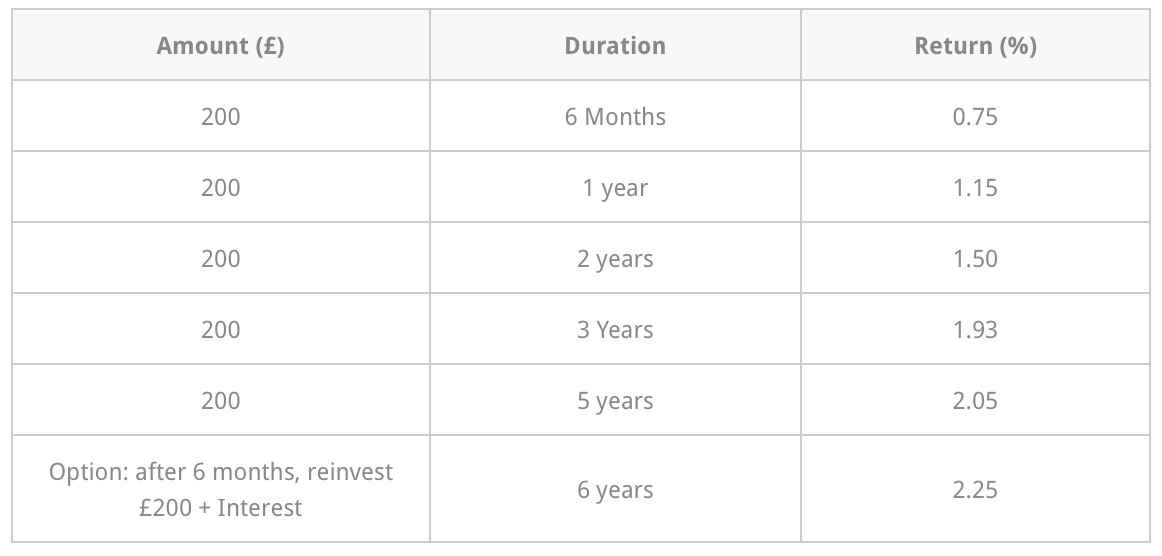

I am actually going to rename these bond trees as they money bloom all year round. Who doesn't like that How a bond ladder worksSay you have £1000 to save. You can either put the whole amount into a single fixed bond for 10 years with a 2.33% return. With this option you will not be able to access any part of the £1000 for the duration of the 10 years. If you feel that this ties you down, you can also opt to create bond ladder. With a bond ladder, you split your £1000 into different amounts across different bonds that mature at different times which also offer varying interest rates as return.  With your £1000 bond ladder, you get the amount you invest back at different times so the first will be £200 + interest after 6 months. You can use that amount to sort our any expenses or you can reinvest it into for example, a 6 year bond to keep the process of building your ladder and getting a guaranteed income each time. As normal with bonds, you'll get the highest interest rate with a longer maturity period. Essentially the issuer or bond provider rewards you more the longer they hold your funds as a loan. If you are retired or you know someone who is about to retire A bond ladder is a good way to manage your savings or lump sum pension while you retain your capital. With a bond ladder, you are guaranteed a monthly (if you bond provides this) income via interest payments across multiple years. Remember Do keep an eye out of the interests you get to ensure that you are getting the types of returns you want. You can also create bond ladders using:

Click here to learn more about bonds.

Back to Blog

Recently I came across the following key words Financial Vulnerability, Financial Capability and Financial resilience. I generally attribute the words vulnerability, capability and resilience to life, emotions and an overall wellbeing. In the articles spewing these words they explored the following how easy is it for you to weather a sudden financial storm? In other words, how ready are you to manage curve balls. In this blog, we discuss the need for a new savings account to cover unexpected however large or small.

Imagine this, two individuals Niya and Hurley receive an email that says you owe £450 from phone contract which you did not formally close if you do now address the cost, it will continue to increase. This is how people become suddenly poor A key goal of WealthSquats to encourage ourselves to build financial resilience, the ability to progress with our financial goals in the face of the unexpected. It is about building a strong finical muscle. What are examples of curve balls |

|  |  |

|  |  |

|  |

Where did I learn my money habits?

9/23/2018

One of my friends asked her dad about how to save and he told her to google it

To unravel this question, we must first understand where individuals learn habits in the first instance? As a child, you learn your speech, behaviors and values from your surroundings which is made up of family and friends. In just the same way you also learn your money habits from your surroundings. Your money habits include how you spend, save and think about money.

“Your money habits include how you spend, save and think about money.”

Your surroundings can have a profound effect on how you manage your money. It also defines your path to wealth. It is therefore critical to assess how much your money habits is attributed to what you have learnt from your surrounding in line with evaluating your current circumstance. This insight will allow you to understand how a family can have wealth for generations, because the rich teach their children rich habits and the less well off teach less well off habits. Teach can also be observation.

Take for example, if you lived in a household where there was always a scramble to pay rent and meet monthly expenses, you could accept this a normal and find yourself with very little to spend at the end of each month as a working adult. But you can make another choice, you can take the time to assess why the scramble took place and plan how you can make money work for you and not fear it.

“Your surroundings can have a profound effect on how you manage your money. It also defines your path to wealth.”

My middle class parents did not teach me about money and financial management. This was in part due to the fact that they did not get an education from their parents. To be frank, money is not a subject that most families or friends discuss in open. To some any topic about money is best held in private or not at all. But if you want to manage money successfully, you need to understand it and you need to talk about it in order to develop successful money habits.

WealthSquats is intended to help others understand that they can start their own path towards financial with the right information, patience and discipline. There is no complex jargon about finance-it is basic, it is simple and it works.

It all starts with knowing that with what you have today, you can make the most of it by starting small.

If you want to manage money successfully, you need to understand it and you need to talk about it in order to develop successful money habits

Take Pleasure in saving money

~Suze Orman

The Pursuit

9/23/2018

Shaking up the plan work hard in school, get a decent job, stay at the job and somehow I would get rich

The plan was to work hard in school, get a decent job, stay at the job and somehow I would get rich. The ‘how’ is something that I struggled with for a long time. Questions I wrestled with include:

- How can I multiply my income

- How can I sustainably save?

- What are other successful people doing that precludes me?

The trigger for Change

The answer to these questions are becoming clearer over time through continuous research and a thirst to get a solid education on managing money. Now, your own quest for wanting to manage your money better can be for several reasons:

- You want to retire early

- You want the capability to afford nice things

- You have goals that you have set for yourself e.g. travel the world, buy a house, buy a car, open a foundation

- You are in debt

- You always have a limited amount of money to survive on at the end of the month

- Other

After much soul searching which included a solo evaluation of my own life's current circumstance and my future goals, I came to understand that getting or being rich was not my goal, my goal was to understand and implement the mechanisms of how to be financially savvy.

Your money management goal may vary from mine and that is a great thing. For you, the exact figure that you need to meet your financial goal is up to you to define.

Let me explain, Financial Independence to me, means that I get to a point in my life where I have enough funds to manage my expenses and address my financial issues without worry. I have always believed that if I do not want to worry, I must have all the necessary information and a solid plan.

In order to plan I needed to know:

- What is my monthly income pre and post taxes?

- What are my monthly and yearly expenses?

- What percentage of my income is saved?

- What percentage of my income is saved?

- How can I budget to have fun?

- What are my goals?

- Why does being financially literate matter to me?

- And more.

With these questions addressed, I was ready to kickstart my journey towards building a more informed life.

About Me:

Age

Millennial

Employment type

Full time

Sector

Information Technology

Indulges in:

Food

Travel

Everything in Ottolenghi

Books

How do I nail down my expenses?

9/22/2018

What is an expense?

An expense is something that takes money away from your pocket. This is my favourite definition provided by Robert Kiyosaki. An expense is in contrast an asset or investments which put money into your pocket (read Rich Dad, Poor Dad).

Taking note of your expenses is about making you aware of what things, actvities, or people that are taking money away from your pocket. The table below provides a sample list of expenses. You can also use this simple spreadsheet to quickly calculate yours.

Types of Expenses |

Description |

Amount I spent per month is.. |

Rent |

Money spent on housing. This should be circa 30% of your monthly income |

... |

Mortgage |

Money spent on owning a home. This should be circa 30% of your monthly income |

... |

Groceries |

Money spent to buy food |

... |

Gym Membership |

Money spent on fitness |

... |

Recreation |

Money spent on socialization including theatre, concerts, dining out, going to the movies etc. |

... |

Electricity/water/gas bill |

Money spent on your home utilities |

... |

Telecom |

Money spent on phone credit, phone payment plans and phone upgrades. |

... |

DSTV/Television |

Money spent on television packages |

... |

Clothing |

Money spent on clothing,bags, shoes,sneakers etc. |

... |

An example of expenses

As part of my research to gain a PHD in understanding money management, I always remember one rule that I carry around. It is called the Millionaire rule which states that Millionaires save or invest 30% of their income after tax and spend 70% on their expenses. This is called the 70:30 rule.

If you are able to save 30% of what you make on a monthly basis in line with the compounding effect you are truly on your path to managing your money.

The 70:30 rule is a guideline for managing your finances. Depending on your situation, you can define what ratio works for you and that can be 80:20 or 75:25. You can even start with 90:10 and then work up to a ratio that you feel comfortable with. The goal here is to ensure that you do not feel strapped or have to struggle to save. If you start to struggle, you will dip into your savings frequently and that is not likely to help you achieve your financial goals.